|

How Can I Benefit from a Charitable Remainder Trust?Sometimes it takes tough economic times and natural disasters to unite and bring out the best in people. Natural disasters such as hurricanes and earthquakes have served to bring communities together and impact the nation as a whole. Americans have given generously to rebuild communities and help local residents through these difficult situations.

Many people have also responded to tragedies worldwide or have made donations to wildlife and environmental charities. And when we give, most of us simply give from the heart and do not always consider the financial implications. In many instances, there are ways to enhance the value of your gifts. The charity can receive a more substantial gift and you can increase your tax benefits. The charitable remainder trust is a popular estate planning strategy that could enable you to gift an appreciated property or security and retain an interest income for you and your family. Once your gift is put in a charitable trust, you may qualify for an income tax deduction on the estimated present value of the remainder interest that will eventually go to charity. Neither party will owe taxes on this transfer or upon the appreciation of the asset. The trust will usually sell the asset and reinvest the proceeds in an income-producing investment. You can receive this income in exchange for gifting the ownership of the asset to the charity. You will then need to decide how you would like to receive income. You can receive either a percentage of the value of the trust or a fixed amount. With a percentage allocation, your income will vary based on the current value of the trust. You can also specify that payments will be made only from income, if that is less than the unitrust amount in any year. You can also provide a “make-up” clause. If the trust is not able to provide the designated income for one year, the shortfall will be made up from income in a later year. Trusts that provide a fixed amount each year will not be able to take advantage of future growth or higher earnings of the asset, but they do offer consistent income even in a stagnating market. Choosing a trustee and clearly stating your intentions in the trust document and to the trustee are of vital importance. Once the trust is in place, it is an irrevocable instrument. Even if the charity does not receive any benefit for several decades, it will eventually assume ownership. In the meantime, the trustee is in charge of controlling the assets in the trust. Choose someone who knows how to handle financial matters and who will carry out your intentions. A charitable remainder trust may allow you to make a substantial gift to charity, avoid capital gains tax, and provide regular income for you and your family. A noncharitable beneficiary is generally taxed on distributions. While trusts offer numerous advantages, they incur upfront costs and ongoing administrative fees. The use of trusts involves a complex web of tax rules and regulations. You might consider enlisting the counsel of an experienced estate planning professional and your legal and tax advisors before implementing such strategies. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2018 Broadridge Investor Communication Solutions, Inc.

1 Comment

How Can I Benefit from a Charitable Lead Trust?Charitable lead trusts are designed for people who would like to benefit a charity now rather than later. You may have heard about some charitable trust strategies before but decided against them because you wanted to make an immediate gift to charity.

With a charitable lead trust, your gift can have an immediate impact, and you’ll be entitled to other benefits as well. These trusts enable you to take advantage of tax benefits and still make a significant gift. If you are accustomed to making outright contributions to your favorite charity, or if you typically sell an investment and give all or a portion of the money to charity, you may be attracted to the special advantages of using a charitable trust. Avoiding capital gains taxes on an appreciated asset is a very appealing benefit for investors. It is also a way for charitable organizations to receive a much larger donation because they are not required to pay tax on capital gains. Once the trust is established and the assets are transferred, the trustee can then sell the assets and reinvest the funds. If you structure the trust as a grantor charitable lead trust, you will be taxed as the owner for federal income tax purposes even though you don't receive the income yourself. You will receive an immediate charitable income tax deduction based on the present value of your gift. Basically, the trust is giving payments to the charity for the duration of the trust but you don't relinquish ownership of the assets. Your income tax deduction will be based on the payments to charity, the duration of the trust, and the IRS interest rate and tables used in the calculation. Your write-off may be limited to a portion of adjusted gross income but can be carried forward to future years. With a charitable lead trust, the income from the reinvested assets will then go to the charity. The charity will receive distributions for the duration of the trust. You may specify that the trust last for a set number of years or the life of you or someone else. At the end of this period, the remaining assets are paid to you or your beneficiaries, for example. A charitable lead trust may also help reduce family squabbles over an inheritance. If you were to actually gift the asset to the charity upon your death, your heirs may feel somewhat cheated. By giving income to the charity during your lifetime and having the remaining assets paid to your beneficiaries upon your death, you may avoid much of this potential controversy. If you are interested in increasing your gift to a charity and your tax benefits during your lifetime, a charitable lead trust may enable you to accomplish your goals. By taking the time to plan your charitable gifts, you may be able to take advantage of some special tax benefits and make charitable giving a real win-win situation. While trusts offer numerous advantages, they incur up-front costs and ongoing administrative fees.The use of trusts involves a complex web of tax rules and regulations. You might consider enlisting the counsel of an experienced estate planning professional and your legal and tax advisors before implementing such strategies. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2018 Broadridge Investor Communication Solutions, Inc. What Gifting Strategies Are Available to Me?

There are a number of different gifting strategies available for planned giving. Each has its advantages and disadvantages. Instead of making an outright gift, you could choose to use a charitable lead trust. With a charitable lead trust, your gift is placed in a trust. The recipient of the gift draws the income from this trust. Upon your death, your heirs will receive the principal with little or no estate tax. If you prefer to retain an income interest in your gift, you could use a pooled income fund, a charitable remainder unitrust, or a charitable remainder annuity trust. With each of these strategies, you receive the income generated by your gift, and the recipient receives the principal upon your death. Finally, you could purchase a life insurance policy and name the charitable organization as the owner and beneficiary of the policy. This would enable you to make a large future gift at a potentially low current cost. The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have contract limitations, fees, and charges, which can include mortality and expense charges. Most have surrender charges that are assessed during the early years of the contract if the contract owner surrenders the policy; plus, there could be income tax implications. Any guarantees are contingent on the financial strength and claims-paying ability of the issuing company. Life insurance is not guaranteed by the FDIC or any other government agency; it is not deposit of, nor is it guaranteed or endorsed by, any bank or savings association. Can I Benefit from an A-B Trust?Married couples have several ways to potentially avoid any estate tax liability when they leave assets to each other.

Because of the unlimited marital deduction, no estate taxes are due when one spouse dies and leaves his or her assets to the survivor (as long as the surviving spouse is a U.S. citizen). However, this may merely postpone taxes that would be due until the death of the second spouse. Federal estate taxes would be owed on the portion of the estate that exceeds the applicable estate tax exemption. The latest major piece of tax legislation is the Tax Cuts and Jobs Act, which was signed into law on December 22, 2017. This Act doubled the federal estate tax exclusion to about $11.18 million in 2018 (indexed annually for inflation). In 2026, the exclusion is scheduled to revert to its pre-2018 level. One basic method to maximize the exemption for both spouses has been an A-B trust (also known as a bypass trust), which preserves the estate exemption of the first spouse to die and also enables the last-surviving spouse to utilize the exemption — essentially doubling the amount exempted from the estate tax. However, with enactment of the American Taxpayer Relief Act of 2012, some couples may no longer need an A-B trust to maximize the estate tax exemption for both spouses. But before you make a decision about the use of a bypass trust, there are a number of issues to consider. First, a little background on the changes in the estate tax as a result of the American Taxpayer Relief Act of 2012. The law permanently extended the higher applicable exemption amount ($5 million, indexed for inflation after 2011) and raised the federal estate tax rate to 40 percent from 35 percent. The increased threshold alone eliminates many people from being subject to the federal estate tax. The act also made permanent "portability" of the exemption to the surviving spouse, which allows surviving spouses to use their spouse's unused exemption plus their own, enabling a couple to exempt up to $22.36 million from federal estate taxes in 2018. However, many states have their own estate or inheritance taxes, or both, and only one state (Hawaii) currently has any portability provisions. This means that when married couples leave all their assets to their spouses, the surviving spouse will be able to use only his or her state estate tax exemption. A trust may preserve a married couple's state estate tax exemption. Additional considerations favoring a trust are the ability to shelter appreciation of assets placed in the trust, to protect assets from creditors, and to benefit children from a previous marriage. HOW AN A-B TRUST WORKSUsing a living trust with an A-B provision (aka A-B or bypass trust), you ensure that both you and your spouse can take advantage of the exemption — once upon the death of the first spouse to die and then again upon the death of the second spouse. When the first spouse dies, two separate trusts are created. The assets of the surviving spouse are transferred to the A trust, and an amount up to the estate tax exemption of the deceased spouse’s assets is transferred to the B trust. This then creates two taxable trusts, each of which is entitled to use the exemption. The B trust is subject to estate taxes. However, because of the applicable exemption, no taxes will be owed. The surviving spouse maintains control of the assets in the A trust and receives income from the B trust. Then, upon the death of the second spouse, only the A trust is subject to federal estate taxes because the B trust was taxed at the first death. After the death of the surviving spouse, the B trust can continue for the benefit of the grantors’ family, often the children. The trust assets can be divided into separate equal trusts for the benefit of the grantors’ children, who will receive net income; and then, at some specified age, they will receive the principal. There are many considerations involved with A-B trusts, including upfront costs and administrative fees. As the use of trusts involves a complex web of tax rules and regulations, you should consider the counsel of an experienced estate planning professional and your legal and tax advisers before implementing such strategies. However, the A-B trust can be an effective way to help reduce estate taxes and preserve family assets. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2018 Broadridge Investor Communication Solutions, Inc. What Is the Capital Gain Tax?

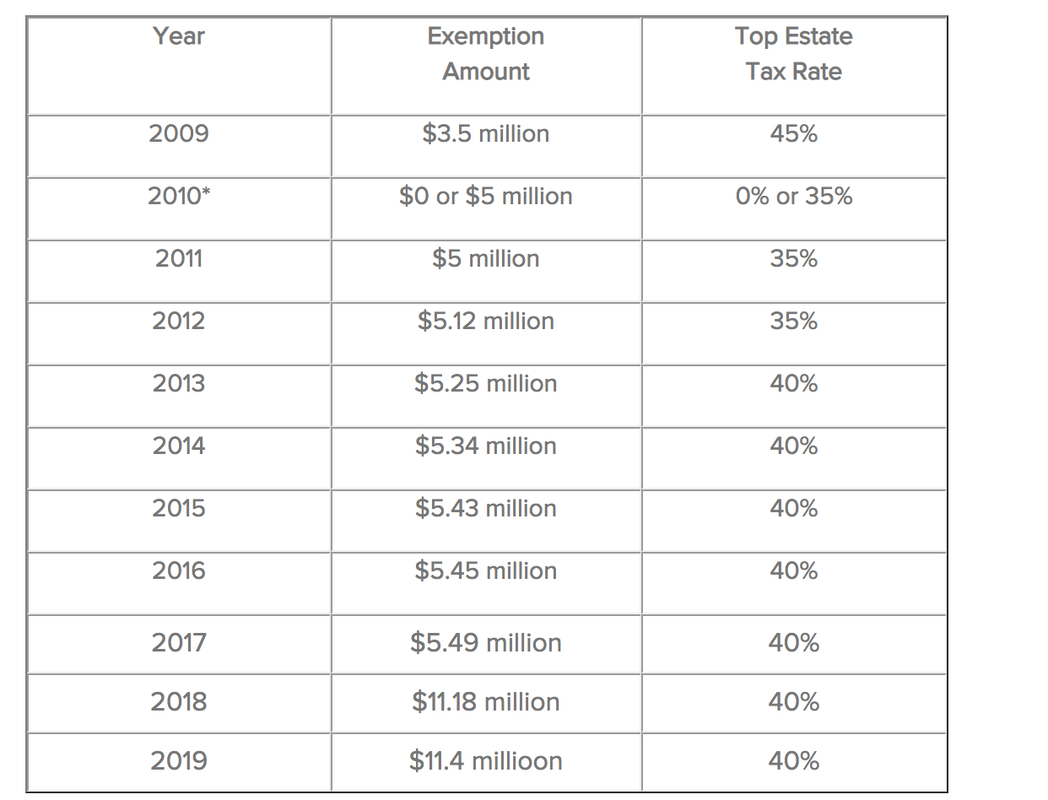

Capital gains are the profits realized from the sale of capital assets such as stocks, bonds, and property. The capital gains tax is triggered only when an asset is sold, not while the asset is held by an investor. However, when a mutual fund sells shares of its holdings during the year, mutual fund investors could be charged capital gains. (A fund’s capital gains distribution is not taxable if the fund is held in a tax-deferred account.) There are two types of capital gains: long term and short term; each is subject to different tax rates. Long-term gains are profits on assets held longer than 12 months before they are sold by the investor. The American Taxpayer Relief Act of 2012 instituted a long-term capital gains tax rate for taxpayers of up to 20%. Short-term gains (on assets held for 12 months or less) are taxed as ordinary income at the seller’s marginal income tax rate. Long-term capital gains are taxed at 15 percent for single filers whose taxable incomes range from $39,376 up to $434,550, and for married joint filers whose taxable incomes range from $78,751 up to $488,850. Lower-income filers pay zero tax on long-term capital gains and dividends. Higher-income filers whose taxable incomes exceed $434,550 for single filers or $488,850 for joint filers pay 20 percent. The taxable amount of each gain is generally determined by a “cost basis” — in other words, the original purchase price adjusted for additional improvements or investments, taxes paid on dividends, certain fees, and any depreciation of the assets. (If you received the property by gift or inheritance, different rules apply to determine your starting basis.) In addition, any capital losses incurred in the current tax year or previous years can be used to offset taxes on current-year capital gains. Losses of up to $3,000 a year may be claimed as a tax deduction for married joint filers and $1,500 for married separately filers. If you have been purchasing shares in a mutual fund over several years and want to sell some holdings, instruct your financial professional to sell shares that you purchased for the highest amount of money, because this will reduce your capital gains. Also be sure to specify which shares you are selling so that you can take advantage of the lower rate on long-term gains. Otherwise, the IRS may assume that you are selling shares you have held for a shorter time and tax you using short-term rates. Capital gains distributions for the prior year are reported to you by January 31, and any taxes owed on gains must be paid by the due date of your income tax return. Higher-income taxpayers should be aware that they may be subject to an additional 3.8% Medicare unearned income tax on net investment income (unearned income includes capital gains) if their adjusted gross income exceeds $200,000 (single filers) or $250,000 (married joint filers). This is an outcome of the Patient Protection and Affordable Care Act. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc. What Is the Federal Estate Tax?The federal estate tax is a tax on property that is transferred to others upon your death. Estate taxes are assessed on the total value of your estate — your home, stocks, bonds, life insurance, and other assets of value — that is over the applicable exemption amount. Everything you own, whatever the form of ownership and regardless of whether the assets have been through probate, is subject to estate taxes. Also referred to as the “death tax,” the federal estate tax was first enacted in this country with the Stamp Act of 1797 to help pay for naval rearmament. After several repeals and reinstatements, the Revenue Act of 1916 put the current estate tax into place. Despite its long history, this tax remains controversial. Estate taxes are calculated on the net value of your estate, which includes all your assets less allowable debts, expenses, and deductions (such as mortgage debt and administrative expenses for the estate). If you have made no taxable gifts, you can estimate the federal estate tax by simply subtracting the applicable estate tax exemption from your taxable estate, and the resulting taxable value is multiplied by 40%, the current federal estate tax rate. The most common exception to the federal estate tax is the unlimited marital deduction. The government exempts all transfers of wealth between a husband and wife from federal estate and gift taxes, regardless of the size of the estate. (The surviving spouse must be a U.S. citizen to qualify for this deduction.) However, when the surviving spouse dies, the estate is subject to estate taxes and, unless the appropriate portability preparations have been made, only the surviving spouse’s applicable exemption can be used. There is also an estate tax deduction for transfers to charity. The Economic Growth and Tax Relief Reconciliation Act of 2001 gradually increased the federal estate tax exemption until finally repealing the federal estate tax altogether for the 2010 tax year only. The 2010 Tax Relief Act reinstated the federal estate tax with a $5 million exemption (indexed annually for inflation after 2011) through December 31, 2012. The 2010 estate tax provisions were made permanent by the American Taxpayer Relief Act of 2012, although the top federal estate tax rate was raised to 40%. The applicable exemption amount in 2017 is $5.49 million. The latest major piece of tax legislation is the Tax Cuts and Jobs Act, which was signed into law on December 22, 2017. This Act doubled the federal estate tax exclusion to $11.18 million in 2018 (indexed annually for inflation) while retaining the 40% tax rate. In 2026, the exclusion is scheduled to revert to its pre-2018 level.  Check with your tax advisor to be sure that your estate is protected as much as possible from estate taxes upon your death. * Executors for estates of decedents who died in 2010 had the option of electing to use the 35% rate, $5 million exemption, and "stepped up" basis of inherited assets for income tax purposes or zero estate tax liability with "carry over" basis of inherited assets for income tax purposes. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc. What Is the Gift Tax?

The federal gift tax applies to gifts of property or money while the donor is living. The federal estate tax, on the other hand, applies to property conveyed to others (with the exception of a spouse) after a person’s death. The gift tax applies to the donor. The recipient is under no obligation to pay the gift tax, although other taxes, such as income tax, may apply. The federal estate tax affects the estate of the deceased and can reduce the amount available to heirs. In theory, any gift is taxable, but there are several notable exceptions. For example, gifts of tuition or medical expenses that you pay directly to a medical or educational institution for someone else are not considered taxable. Gifts to a spouse who is a U.S. citizen, gifts to a qualified charitable organization, and gifts to a political organization are also not subject to the gift tax. You are generally not required to file a gift tax return unless the total gifts to a recipient exceed the annual gift tax exclusion for that calendar year. The Tax Cuts and Jobs Act, which was signed into law on December 22, 2017, increased the Gift tax in 2018 to $15,000 and remains at $15,000 for 2019. The exclusion amount iindexed annually for inflation. A separate exclusion is applied for each recipient. In addition, gifts from spouses are treated separately; so together, each spouse can gift an amount up to the annual exclusion amount to the same person. Spouses can also elect to split gifts so that all gifts made by either spouse during a year are treated as made one-half by each spouse. This enables both spouses' annual gift tax exclusion to be used. However, you must file a gift tax return to split gifts with your spouse. Gift taxes are determined by calculating the tax on all gifts made during the tax year that exceed the annual exclusion amount, and then adding that amount to all the gift taxes from gifts above the exclusion limit from previous years. This number is then applied toward an individual’s lifetime applicable exclusion amount. If the cumulative sum exceeds the lifetime exclusion, you may owe gift taxes. The 2010 Tax Relief Act reunified the estate and gift tax basic exclusion amount at $5 million (indexed for inflation), and the American Taxpayer Relief Act of 2012 made the higher exemption amount permanent while increasing the estate and gift tax rate to 40% (up from 35% in 2012). The latest major piece of tax legislation is the Tax Cuts and Jobs Act, which was signed into law on December 22, 2017. The Tax Cuts and Jobs Act doubled the federal estate tax exclusion to $11.18 million in 2018 (indexed annually for inflation); in 2026, the exclusion is scheduled to revert to its pre-2018 level.This enables individuals to make lifetime gifts of $11.18 million before the gift tax is imposed. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc. How much money can I put into my IRA or employer-sponsored retirement plan?IRAs and employer-sponsored retirement plans are subject to annual contribution limits set by the federal government. The limits are adjusted periodically to compensate for inflation and increases in the cost of living.

IRASFor tax year 2018 the IRA contribution limit was $5,500, for 2019 you can contribute up to $6,000 to all IRAs combined (the limit is adjusted annually for inflation). If you have a traditional IRA as well as a Roth IRA, you can only contribute a total of the annual limit in one year, not the annual limit to each. If you are age 50 or older, you can also make a $1,000 annual “catch-up” contribution. EMPLOYER-SPONSORED RETIREMENT PLANSEmployer-sponsored retirement plans such as 401(k)s and 403(b)s have an $19,000 contribution limit in 2019 (a cost-of-living increase of $500); individuals aged 50 and older can contribute an extra $6,000 each year as a catch-up contribution. (Section 403(b) and 457(b) plans may also provide special catch-up opportunities.) SIMPLE PLANSYou can contribute up to $13,000 to a SIMPLE IRA or SIMPLE 401(k) plan in 2019, and an extra $3,000 catch-up contribution if you are age 50 or older (unchanged from 2018). Distributions from traditional IRAs and most employer-sponsored retirement plans are taxed as ordinary income, except for any after-tax contributions you've made, and the taxable portion may be subject to 10% federal income tax penalty if taken prior to reaching age 59½ (unless an exception applies). If you participate in both a traditional IRA and an employer-sponsored plan, your IRA contributions may or may not be tax deductible, depending on your adjusted gross income. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc. What Is a Required Minimum Distribution?A required minimum distribution (RMD) is the annual amount that must be withdrawn from a traditional IRA or a qualified retirement plan (such as a 401(k), 403(b), and self-employed plans) after the account owner reaches the age of 70½. The last date allowed for the first withdrawal is April 1 following the year in which the owner reaches age 70½. Some employer plans may allow still-employed account owners to delay distributions until they stop working, even if they are older than 70½.

RMDs are designed to ensure that owners of tax-deferred retirement accounts do not defer taxes on their retirement accounts indefinitely. You are allowed to begin taking penalty-free distributions from tax-deferred retirement accounts after age 59½, but you must begin taking them after reaching age 70½. If you delay your first distribution to April 1 following the year in which you turn 70½, you must take another distribution for that year. Annual RMDs must be taken each subsequent year no later than December 31. The RMD amount depends on your age, the value of the account(s), and your life expectancy. You can use the IRS Uniform Lifetime Table (or the Joint and Last Survivor Table, in certain circumstances) to determine your life expectancy. To calculate your RMD, divide the value of your account balance at the end of the previous year by the number of years you’re expected to live, based on the numbers in the IRS table. You must calculate RMDs for each account that you own. If you do not take RMDs, then you may be subject to a 50% federal income tax penalty on the amount that should have been withdrawn. Remember that distributions from tax-deferred retirement plans are subject to ordinary income tax. Waiting until the April 1 deadline in the year after reaching age 70½ is a one-time option and requires that you take two RMDs in the same tax year. If these distributions are large, this method could push you into a higher tax bracket. It may be wise to plan ahead for RMDs to determine the best time to begin taking them. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc. What are the tax benefits of charitable trusts?Americans give freely to support the causes they value, from churches, education, and the arts to medical research. Fortunately, current tax laws encourage and even reward philanthropy. Beyond the basic tax deductions for charitable giving, setting up one or both of the following types of trusts could provide financial advantages in addition to the personal satisfaction that comes from giving.

CHARITABLE REMAINDER TRUSTWhen money, securities, property, or other assets are placed in a properly structured charitable remainder trust, the grantor or the grantor's beneficiaries receive payment of a specified amount at least annually. When the trust expires, the designated charity receives the assets that remain. For the grantor, there are a few potential tax benefits: (1) Assets placed in the trust may qualify for an income tax deduction on the estimated present value of the remainder interest that will eventually go to charity. (2) At death, trust assets are not subject to estate taxes because they are no longer part of the grantor’s taxable estate. (3) Any appreciated assets in the trust are also exempt from current capital gains tax. CHARITABLE LEAD TRUSTA charitable lead trust is an estate conservation tool that uses the grantor’s assets to provide income to a charity. At the end of the trust period, the remaining assets are paid to the grantor or the grantor's beneficiaries. This type of trust could potentially reduce the estate tax due upon death, most notably on highly appreciated assets, because they are not subject to current capital gains tax. Keep in mind that donations to both types of charitable trusts are irrevocable. This means that the assets cannot be withdrawn once the trust is formed. Also bear in mind that not all charitable organizations are able to use all possible gifts. It is prudent to check first. The type of organization selected can also affect the tax benefits that may be received. When structured properly, these tools could possibly be used to benefit the charities of your choice and also help to reduce your tax obligations at the same time. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional and your legal and tax advisors before implementing such strategies. Trusts incur upfront costs and ongoing administrative fees. The information in this newsletter is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc. |

Archives

January 2019

Categories

All

|

RSS Feed

RSS Feed

|

|

Contact Us

|

© 2024 Sunshine Financial Solutions of South Florida, Inc.

Securities offered through OneAmerica Securities, Inc., a Registered Investment Advisor, member FINRA SIPC. Sunshine Financial Solutions of South Florida, Inc. is not an affiliate of OneAmerica Securities or the companies of OneAmerica and is not a broker dealer or Registered Investment Advisor. Provided content is for overview and informational purposes only and is not intended and should not be relied upon as individual tax, legal, fiduciary, or investment advice. Neither OneAmerica Securities, the companies of OneAmerica, or Sunshine Financial Solutions of South Florida, Inc. provide tax or legal advice. For answers to specific questions and before making any decisions, please consult a qualified attorney or tax advisor. Guarantees are subject to the claims paying ability of the issuing insurance company.

Securities offered through OneAmerica Securities, Inc., a Registered Investment Advisor, member FINRA SIPC. Sunshine Financial Solutions of South Florida, Inc. is not an affiliate of OneAmerica Securities or the companies of OneAmerica and is not a broker dealer or Registered Investment Advisor. Provided content is for overview and informational purposes only and is not intended and should not be relied upon as individual tax, legal, fiduciary, or investment advice. Neither OneAmerica Securities, the companies of OneAmerica, or Sunshine Financial Solutions of South Florida, Inc. provide tax or legal advice. For answers to specific questions and before making any decisions, please consult a qualified attorney or tax advisor. Guarantees are subject to the claims paying ability of the issuing insurance company.